Welcome to the new subscribers that have joined us over the last week. The aim of this newsletter is to help you navigate the world of crypto. There’s an incredible amount of information out there so we try to distil it into the things you MUST know each week, covering both macro and crypto.

For snippets and analysis on institutional crypto trading, give our X account a follow HERE.

Onto the newsletter. Here’s what you’re getting this week:

Macro Update: Our latest view on the macro and its impact on crypto markets.

Crypto Native News: Kraken releases its Q2 results, JP Morgan and Coinbase partner.

Institutional Corner: Visitors to South Korea can use crypto kiosks to convert stablecoins to cash, Bolivia signs agreement with El Salvador, Algeria bans all crypto relayed activities, Robinhood posts its Q2 results.

Charts of the Week: DeFi sector TVL hits 3 year high, Bitcoin 1% market depth continues to climb, open interest in IBIT more than tripled so far this year, PancakeSwap has the highest DEX volume.

Top Jobs in Crypto: Featuring Galaxy, XBTO, Keyrock, Blockchain.com, Avenir Group and Berenberg.

Macro Update

This is where we connect the dots between macro and crypto.

Fiscal Dominance and Treasury QE

Renewed tariff and recession fears saw equities reverse much of the July gains, in an action packed macro week.

In what has been the worst week for equities since the tariff-driven sell off in early April, Bitcoin and the wider crypto space was also dragged lower, despite still recording solid gains on the month. This was especially the case with ETH which has found renewed vigour with the passing of the GENIUS act (positive for stablecoin growth for which ETH is the predominant settlement layer) and the emergence of several large corporate ETH treasury strategies akin to the Michael Saylor Bitcoin playbook. Even with this correction, ETH is up over 40% since the end of June 🔥

Despite some market friendly deals with the likes of the EU and Japan and importantly a temporary reduction in tariffs with China as talks progress, uncertainty into the August 1st tariff deadline weighed on sentiment.

We continue to look through the tariff “noise” as Trump simply uses them as a negotiation tactic and we expect the net impact on growth and inflation to be minimal. Indeed, Trump himself said on signing the order (and pushing back the start date to 7th August) that “It doesn’t mean that somebody doesn’t come along in four weeks and say we can make some kind of a deal.” Nonetheless, markets hate uncertainty and the resulting uncertainty was sufficient to put a dent in risk.

Too late JPow?

Adding a one-two punch to the tariff uncertainty however was a combination of a hawkish JPow at the latest Fed meeting followed by a weak US jobs report which reignited some recession jitters.

The Fed held rates steady at 4.25%-4.5% as expected although notably two members dissented, voting to cut rates 25bps and the statement noted that “economic activity moderated in the first half of the year.” However, in a more hawkish press conference, JPow noted inflation remained above the Fed’s target and reiterated the central bank’s willingness to wait for more data before making another cut. Thursday’s release of the Fed’s preferred inflation gauge, core PCE, remaining at 2.8% underscored the Fed’s caution, whilst Q2 GDP coming in at 3% (albeit driven by a large drop in imports) appeared to support the “wait and see” approach.

Markets consequently started to price out a September rate cut. However, Friday’s US employment report showed the US economy only added 73k jobs in July, below estimates of 115K. More concerning was the downward revisions to May and June which were a combined 258k lower than initial estimates. This was the largest downward adjustment outside of recession periods since 1968 🤯 The 3 month total of jobs created is just 106k, a much cooler labour market the Powell appeared to think on Wednesday.

Quickly markets moved to price back odds over 80% of a September rate cut, yet despite the significant move lower in yields, some 20bps lower across the curve, recession fears and a sense that the Fed are behind the curve weighed heavily on risk into the weekend. Trump subsequently firing the commissioner responsible for compiling the jobs data at the BLS doing little to assure investors of the credibility of the US and integrity of the data!

Still, despite events of the past week, little has changed to dent the “goldilocks” narrative we have been championing here for the past few months. The US economy is clearly showing signs of underlying softness and labour market weakness, yet it's a slowing, not collapsing economy. Inflation is sticky but not accelerating. With this report likely to have increased the risks to the employment side of the mandate, the Fed now has a pass to cut rates in September.

Fiscal dominance…

Yet, the Fed is not the driver of risk right now as Trump and Bessent are maintaining the Biden “fiscal dominance” playbook, continuing to run deficits north of 6%. Whilst that continues, growth will remain resilient and keep slowing the pace of the rate cutting cycle, which we believe will extend the typical 4 year Bitcoin cycle.

What matters more is how these deficits are funded and the resulting impact on market liquidity. To that end, more important for us last week was the Quarterly Refinancing Announcement delivered on Wednesday.

The borrowing requirement for the next two quarters in the US is a mind blowing $1.6 trillion, with circa $1 trillion being raised in Q3 😳 As someone pointed out on X, the 2008 financial crisis bailout package in the US was $800bn. We’re effectively funding a financial crisis bailout every quarter. Nothing stops this train!

Importantly though, the US Treasury is doubling down on short-term debt issuance, reviving the Yellen-era playbook that Scott Bessent once criticised. The debt will be funded by leaning heavily on Treasury bills that mature in less than a year. The auction sizes of longer-dated bonds, meanwhile, will remain unchanged for "several quarters." It’s a debt strategy designed to keep longer-end yields pinned—protecting interest rate-sensitive sectors like housing and consumer credit—even as the government’s fiscal needs balloon.

This is effectively a form of “Treasury QE” or pseudo Yield Curve Control (YCC) which keeps longer dated yields artificially low and this form of financial repression drives the debasement of the dollar. It also risks pushing up front end yields which would then force the Fed to provide liquidity into the front end in a “not QE QE” type monetary operation, as they were forced to in the repo blow up in 2019, to maintain front end rates which are consistent with where the Fed funds rate is set.

Dips are your friend…

Stepping back then, we see little reason to change our bullish view of the world and continue to see equities and Bitcoin making new record highs over the following few months. There was some skittishness coming into August given general seasonal weakness for markets over the August/September summer lull. Trump delivering trade deals that relatively favour the US over its trading partners has also seen the dollar rally in July (although we reversed somewhat post the soft US data on Friday) - we have written how important a factor the dollar sell off this year has been in propelling risk higher.

However, the dollar impact, outside of short term knee-jerk reactions, tends to act with a 3 month lag. If July was to mark the lows for the dollar, then we wouldn’t expect a stronger dollar to start to materially impact until October/November time. However, we are still of the view that the dollar has been managed lower as part of these trade negotiations and with the renewed fears around the strength of the US economy, we believe the dollar could have further to fall.

Either way, whilst it's understandable some risk may have been taken off the table after such a stellar run, we see this more as a shallow, short term correction with another leg higher for risk ahead of us into November.

To reiterate, the hugely positive drivers for these markets remain firmly in place and will be difficult for bears to sustainably get in the way of:

Rising global liquidity ✅

Global rate cutting cycle ✅

Lagged pass through from a weak dollar ✅

US fiscal dominance and rising deficits ✅

“Treasury QE” and artificially suppressed yields ✅

Tariff and geopolitical fears fading into the background ✅

Meanwhile, whilst we see this as a broadly supportive backdrop for risk generally, the positive idiosyncratic drivers for crypto continue apace. BTC and ETH continue to digest some supply as profits are taken after recent gains yet with inflows both via the ETF’s and corporate treasuries, there remains a powerful demand/supply dynamic which we expect to keep this bull market intact. Indeed, we think its reasonable to expect BTC to begin its ascent to 150k over the coming few months and ETH to make new record highs and break above 5k.

These dips in bull markets are your friend. Keep stacking 💪

Native News

Key news from the crypto native space this week.

Crypto exchange Kraken released its Q2 results this week. The firm reported $411.6 million in revenue in the second quarter of this year, up 18% year-on-year, while its adjusted EBITDA fell 7% to $79.7 million. Kraken's total exchange volume grew 19% year-over-year to $186.8 billion in the second quarter, though it declined 11% from the previous quarter. Assets on the platform expanded 47% year-on-year to reach $43.2 billion at the end of the second quarter. Kraken also noted that its share of stable-fiat spot volumes grew from 43% to 68% in the second quarter. The statement from Kraken noted that "After a strong Q1, there was market turbulence related to U.S. tariffs and broader macro uncertainties. Q2 volumes decelerated quarter-over-quarter, as Q2 tends to be a seasonally lower quarter for trading activity across the industry." Read more details from Kraken HERE.

JPMorgan announced a partnership with Coinbase to roll out a series of integrations aimed at making it easier for the bank’s 80 million customers to buy crypto. The partnership will allow JPMorgan customers to directly connect their bank accounts to Coinbase, redeem Ultimate Rewards points for USDC, and use credit cards to fund crypto purchases. In a phased integration, Credit card support is expected to launch this fall, while rewards redemption and bank account linking are slated for 2026. Coinbase said this marks the first time a major U.S. credit card rewards program can be used to buy crypto. Chase customers will be able to convert points at a rate of 100 points to $1 in USDC on Coinbase’s Base blockchain. Read full details from Coinbase HERE.

Institutional Corner

Top stories from the big institutions

Foreign visitors to South Korea can now use select crypto-enabled kiosks to convert stablecoins into cash. They are available at major tourist and retail sites but access is limited to foreign passport holders under regulatory sandbox rules. Built and operated by South Korean blockchain firm DaWinKS in partnership with the Kaia DLT Foundation, the machines support Kaia-issued USDT, a version of Tether’s stablecoin on the public blockchain formed from the merger of Klaytn and Finschia, two projects backed by Korean tech giant Kakao and Japan’s LINE app. The companies say the machines are visible, easy to use, and integrated with infrastructure Koreans already rely on, such as convenience stores and transit hubs. Verified users can withdraw fiat in 85 currencies or load funds onto a local transit card.

On Wednesday, Bolivia signed a formal cooperation agreement with El Salvador’s Comisión Nacional de Activos Digitales (CNAD) which aims to help Bolivia develop regulatory frameworks, monitoring tools, and legal standards for digital assets. The Central Bank of Bolivia (BCB) and El Salvador’s Comisión Nacional de Activos Digitales (CNAD) will collaborate on a broad range of crypto policy initiatives under the terms of a newly signed memorandum of understanding. The agreement includes joint work on blockchain intelligence tools, regulatory frameworks, and risk analysis models. It is open-ended and takes effect immediately. According to figures released by the BCB, digital asset transaction volume grew from $46.5 million in June 2024 to $294 million in June 2025, a more than sixfold increase following the passage of Decree No. 082/2024, which authorised broader use of cryptoassets across the country.

The Algerian government has introduced a new law explicitly banning all crypto-related activities, including trading, ownership and mining. Enacted on July 24, the legislation expands and extends the 2018 Financial Law, which prohibited the holding and exchange of cryptocurrencies but didn’t cover mining activities. The scope of the law covers all potential activity involving cryptocurrencies, extending to issuance and promotion, as well as the offering of crypto-trading services. Violations could be met with prison sentences of between two to 12 months, and/or a fine between 200,000 and 1 million dinars (c. $1,500 to $7,700).

Robinhood posted its Q2 earnings this week, beating analyst expectations. The retail brokerage posted $989 million in total sales, up 45% from a year ago and surpassing analysts’ expectations of $913 million. With an earnings per share mark of $0.42, Robinhood reported $386 million in second-quarter profits, up $50 million year-over-year and beating analyst expectations of $276.6 million. Robinhood said that it generated $160 million in crypto trading revenue during the second quarter, a 98% increase from a year ago. However, the figure fell quarter-over-quarter from $252 million. The company’s stock price has risen 184% year-to-date, outperforming crypto-native competitors like Coinbase, whose shares have jumped 51% to $375 over the same period of time.

Charts of the Week

Because charts are just as important as macro.

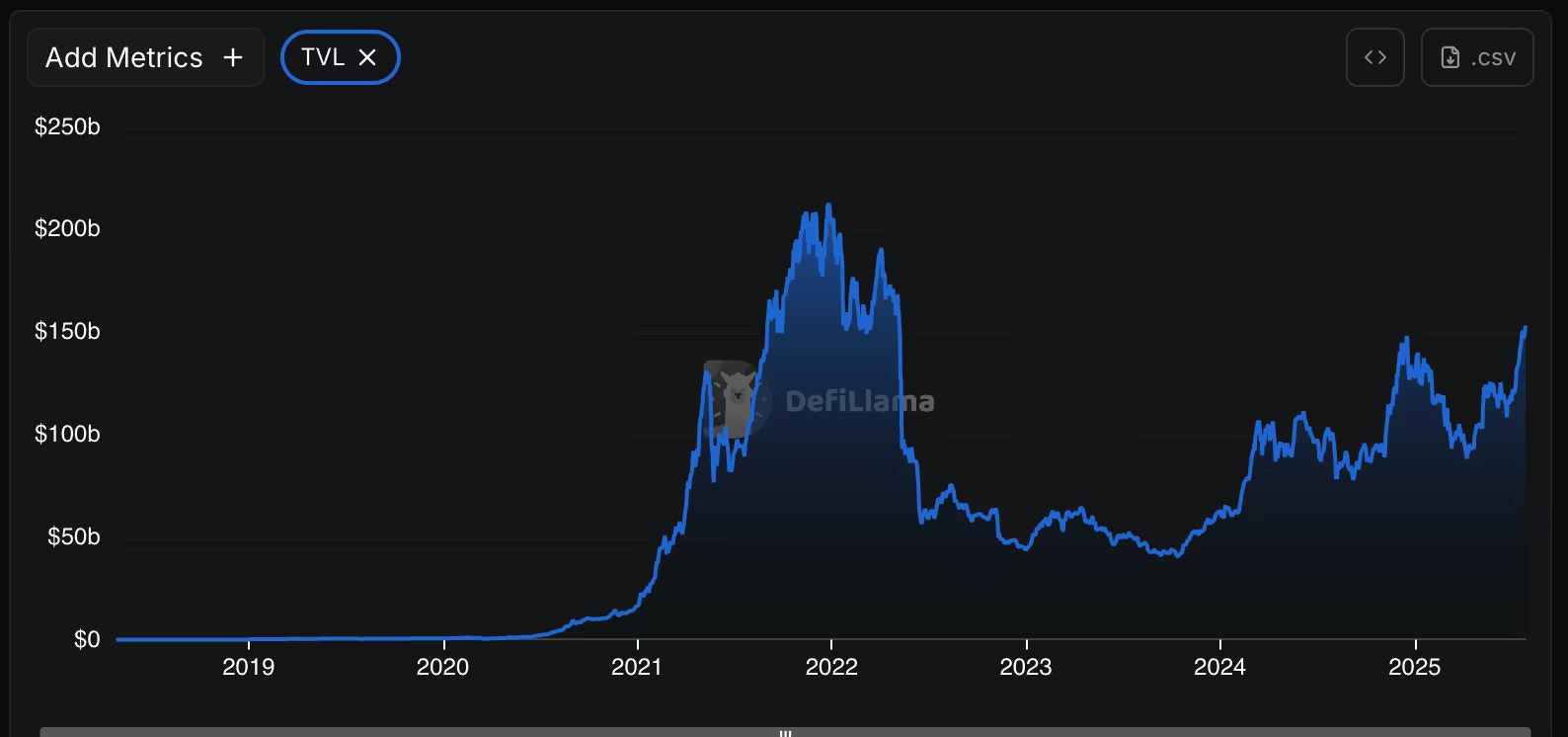

DeFi sector TVL hit a 3-year high of $153B, with Ethereum leading nearly 60% of the market share.

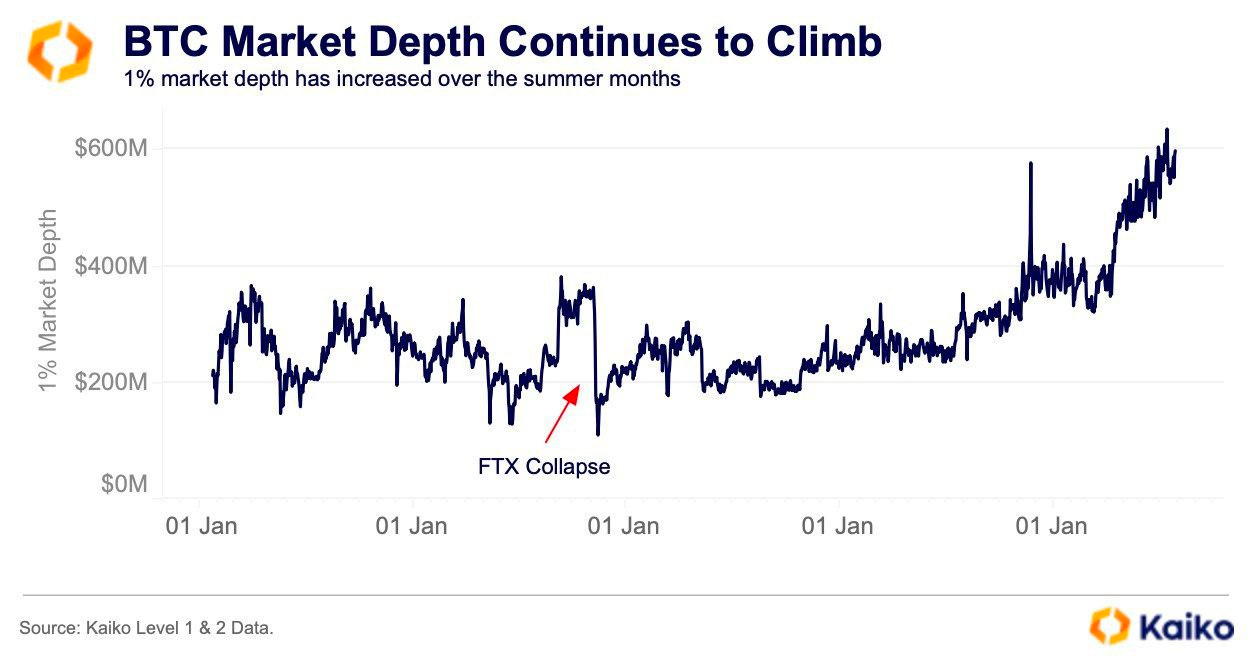

Bitcoins 1% market depth has increased over the summer months

Open interest in IBIT-linked options has more than tripled this year to around $34 billion. Daily volumes has averaged $4 billion in recent trading, surpassing large funds in credit and emerging markets.

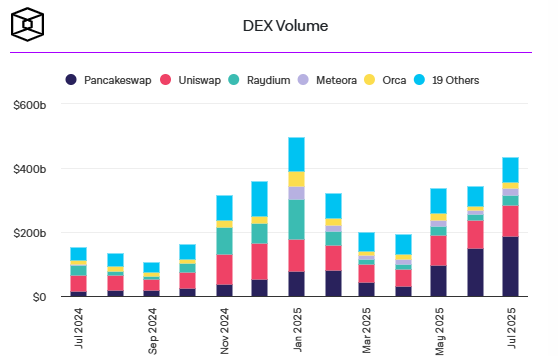

PancakeSwap recorded $151 billion in spot trading volume in June, accounting for over 43% of all spot DEX trades. Hat tip to The Block for the chart.

Top Jobs in Crypto

Well, we all want to work in Crypto don’t we. Here’s a bit of help on your job search!

Director of Sales Europe at GK8 by Galaxy

Private Credit Analyst at XBTO

Options Trader - Digital Assets Market Making at Keyrock

OTC Crypto Trader at Blockchain.com

Options Trader Crypto at Avenir Group

Business Analyst Digital Assets at Berenberg

DISCLAIMER: The content in this newsletter is not financial advice. This newsletter is strictly educational and is not investment advice or a recommendation to buy or sell any assets or to make any financial decisions. Crypto markets are volatile, please be careful and do your own research.

Team - great recap as always. Thanks.

Any related meetups planned in London?