Connecting the Dots

Episode 57 - January Sales Are Ending

Welcome to the new subscribers that have joined us over the last week. The aim of this newsletter is to help you navigate the world of crypto. There’s an incredible amount of information out there so we try to distil it into the things you MUST know each week, covering both macro and crypto.

For snippets and analysis on institutional crypto trading, give our Twitter a follow HERE.

If you think someone will benefit from reading this newsletter, we’d be really grateful if you could share it with them. Thanks!

Onto the newsletter. Here’s what you’re getting this week:

Macro Update: Central bank speakers providing some headwinds for crypto, so far so good on the bitcoin ETF’s. The broad macro environment continues to look supportive for Bitcoin and wider crypto.

Crypto Native News: Tether continues to buy bitcoin with profits, Hidden Road adds listed derivatives to its product suite, Binance sees net inflows, Coinbase were in court and dYdX becomes the largest DEX by volume.

Institutional News: EU regulation forces crypto firms to run due diligence on their customers, Donald Trump says he would never allow a CBDC and Hong Kong to have a spot bitcoin ETF.

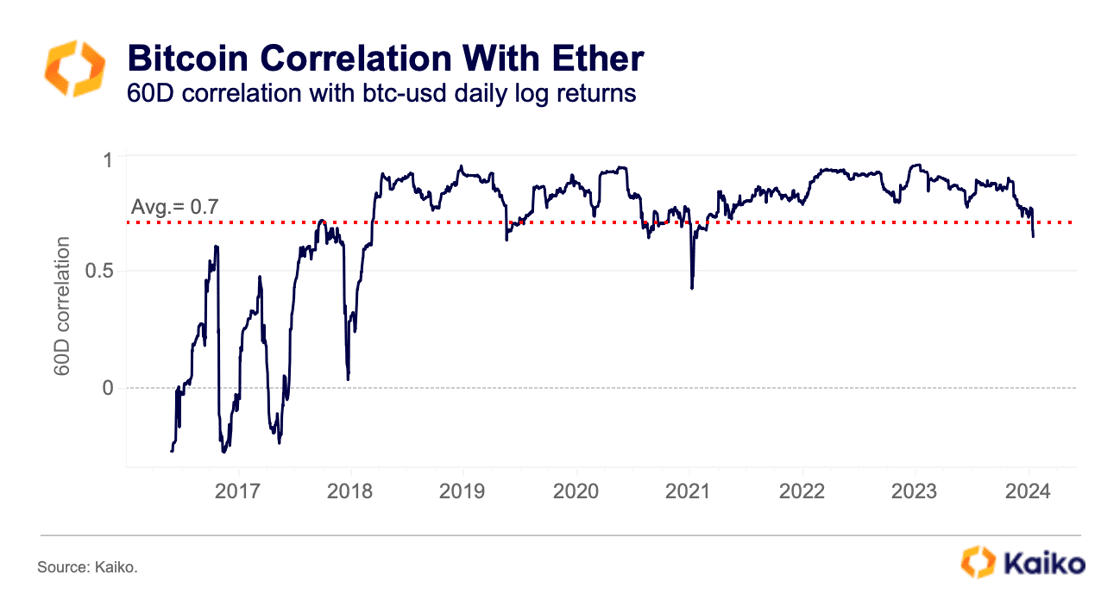

Charts of the Week: BTC:ETH correlation drops, outperformance of S&P vs cash, cash injections at large banks trending up and MSCI China index going negative.

Top Jobs in Crypto: Featuring Hudson River Trading, Revolut, MoonPay, Coinbase, Komainu and Blockchain.com

Macro Update

This is where we connect the dots between macro and crypto.

January Sales are Ending

A mixed macro picture this week failed to prevent the S&P 500 and Nasdaq clocking new record highs, despite the chorus of central bankers, led by the Fed’s Waller, trying to temper rate cut expectations.

Waller sparked a sell off in rates with comments on Tuesday in which he said “I see no reason to move as quickly or cut as rapidly as in the past” given the current resilience of the US economy. Of course, the reason past rate cuts came “quickly and rapidly” was because Fed members at the time also saw little reason to cut quickly and rapidly! No Fed member can see the car crash ahead whilst looking at the rear-view mirror as they drive.

The ECB’s Lagarde meanwhile, despite seeing the German economy car crash ahead, which saw GDP shrink 0.3% in the final quarter of 2023, expects she has more time to tap the breaks than the market thinks, saying it was “likely” rate cuts come in the summer and not in spring as currently priced.

The push back from central bankers subsequently drove a re-pricing of rate cut expectations and the front end led a broad based bond sell off, with 10yr US yields hitting just shy of 4.20% before reversing to close at 4.12% on Friday. This also drove the broad dollar higher, although the move faded into the latter part of the week.

All of this provides somewhat of a headwind to crypto, which continues to struggle for direction post the spot BTC ETF launch as positions adjust and Grayscale selling battles the new inflows into the ETF’s. Volatility consequently being driven lower as we trade in a relatively narrow range in the low 40k’s. However, the subdued price masks the phenomenal debut the spot ETF’s have made. As Bloomberg’s Eric Balchunas points out, Friday’s $1.2bn traded volume for the nine ETF’s (ex Grayscale) puts them in the top 1% of volume for all ETF’s. It’s just a matter of time before the Grayscale selling completes and total AUM starts to climb and in our view rival some of the biggest ETF’s in the world. The large institutional money always moves slowly, but so far, so good.

Whilst the market is in the early-year sparring, trying to establish a coherent narrative across asset classes, there’s little to change or concern our bullish view of the world as it relates to risk and crypto.

The broad disinflation narrative continues to hold, with China emitting a strong global deflationary pulse, whilst the lagged impact of the aggressive rate hikes from major central banks should hit in earnest throughout this year. Interestingly, Trueflation’s real time measure of inflation in the US now sits at 1.85% Vs the official (backward looking) rate of 3.4%. Meanwhile, Japan’s core CPI fell to 2.3%, down from 2.5% and the lowest since June 2022, supporting our view that the BoJ will unlikely have much room to “normalize” policy and cause the bond market disruption the bond vigilantes continue to excite about.

Global liquidity also looks set to continue upwards, with QT to be tapered in the US, whilst China has little choice but to pump the liquidity hose and artificially inflate domestic assets as property and stocks continue their downward spiral. Indeed, last week saw the PBOC inject an above forecast 995bn Yuan into the system via the medium term lending facility, whilst some brokerages suspended short selling.

To gauge the scale of the problems in China (the world’s second largest economy let's remember) they also announced a proposal to issue 1trn Yuan ($139bn) of new, ultra long debt, under a special sovereign bond plan. This will be only the 4th such sale in 26 years with other times being in 1998 in the aftermath of the Asian financial crisis and more recently in 2020 to pay for pandemic response measures.

Major fiat economies continue to battle the pandemic of debt with the antidote being more debt, more liquidity, more currency debasement.

All in all, we remain on track with the unfolding macro. A disinflationary environment, with major central banks set to start cutting rates. Whilst uncertainty remains over the timing and the depth of cuts, the direction of travel is clear and over the course of the year will provide a tailwind to markets.

Shorter term, the bond sell off is a concern and 4.20% in 10yr yields is a level worth watching as a break above and a more disorderly bond sell off has the potential to weigh on broad risk which currently is riding the liquidity wave and shaking off the bond market volatility (although we continue to see bond yields heading lower over the course of 2024).

Bitcoin however may prove less sensitive if higher yields re-ignites debt sustainability fears and resumes its “flight to quality” narrative. This was perhaps one of the biggest “narrative” developments for Bitcoin in 2023 and now means that Bitcoin captures both the left and right tails of the risk probability distribution. Outperforming in the broad liquidity driven risk-on for high beta assets (the right tail) and outperforming in the risk-off flight to quality (left tail) where US bonds are no longer perceived as the safe haven, “quality asset.”

The broad macro environment continues to look supportive for Bitcoin and wider crypto. Grayscale selling should start to abate and be overpowered by the inflows into spot ETF’s and the subsequent demand/supply mismatch points to more explosive moves to the topside. Short term leveraged longs have likely been liquidated and the recent caution post the ETF launch, with a building consensus that we see prices sub 40K, perhaps suggests the market is now under-positioned and the path of pain would be a continuation of the move higher. We were asked frequently ahead of the ETF approval if the event was “priced”, of which we felt the headline announcement clearly was. Now, it feels the market is under pricing the both demand/supply mismatch resulting from the ETF’s, as well as the positive macro tailwinds.

The January sales are coming to an end.

Native News

Key news from the crypto native space this week.

According to on-chain analytics, stablecoin issuer Tether bought $380 million of bitcoin at the end of last quarter, bringing its total holdings to 66,465 BTC. Starting in September 2022, Tether has been consistently acquired bitcoin every quarter. Its second-largest purchase was in March 2023 when it bought 15,915 BTC. The most recent purchase of 8,888 BTC, at the end of Q4 2023, stands as Tether's third largest to date.

Hidden Road, the global credit network for institutions, today announced that it has extended its credit intermediation, clearing and financing offerings to cover listed derivatives markets through the firm’s U.S. entity, Hidden Road Partners CIV US LLC, a registered futures commission merchant (FCM). The listed derivatives business is starting with CME Clearing as its first venue and will be expanding venue and clearinghouse coverage globally over the coming months. Alex Kallelis, Head of Business Development, Americas said “Extending our services to cover listed derivatives is a significant step in our mission to provide comprehensive clearing across venues, products and asset classes,” “Operating as an FCM clearing member of CME Clearing enables more efficient market access for our clients across a full spectrum of traditional and digital asset classes.” Read the full press release HERE.

Since the multi billion fine back in November 21, Binance has seen net inflows of $4.6bn. That has outpaced some of the exchange rivals, including OKX ($2.6bn inflows and Bybit ($1.1bn inflows). $3.5bn of the inflows have come in January, which is more than any whole month inflow since November 2022. As a reminder, and as part of the settlement agreements, new Binance CEO Richard Teng is tasked with establishing a global headquarters, appointing a board and appointing an independent monitor for 3 years.

New York District Judge Katherine Polk Failla probed Coinbase in court on Wednesday about whether tokens listed on its exchange were securities. Coinbase was sued by the Securities and Exchange Commission in June for allegedly operating as an unregistered exchange, broker and clearing agency. Coinbase has pushed back on those claims, arguing for the case to be dismissed and accusing the regulator of taking a "regulation by enforcement approach." Coinbase lawyer William Savitt delved into how securities are defined, marking what they say is a difference between "investing in Beanie Baby Inc. and buying Beanie Babies." From its June complaint, the SEC had said tokens including SOL, ADA, MATIC, FIL, SAND, AXS, CHZ, FLOW, ICP, NEAR, VGX, DASH and NEXO were securities. Savitt noted that Coinbase does not claim blockchain tokens can never be deemed securities. He added "We don’t take the view that token transactions can never be investment contracts," adding that, the SEC did not present any allegations in its lawsuit that would satisfy the investment contract definition.

dYdX has overtaken Uniswap as the largest DEX by daily trading volume. dYdX made a strategic migration from Ethereum to Cosmos and subsequently activated full trading under the new infrastructure. According to data from CoinMarketCap, the v4 version of dYdX on Cosmos recorded $542.5 million in trading volume over a 24-hour period, outpacing Uniswap v3's $464 million. The DEX now holds 10.7% of all the crypto market share.

Institutional Corner

Top stories from the big institutions

Policymakers in the European Union reached a provisional deal on parts of a regulatory package to combat money laundering, which will force crypto firms to run due diligence on their customers. The Anti-Money Laundering Regulation (AMLR) is a broad-stroke effort to combat sanctions evasion and money laundering. The European Parliament and Council (which gathers finance ministers from the bloc's 27 member states) have agreed to measures, including for crypto firms to apply "customer due diligence measures when carrying out transactions amounting to €1,000 (approx. $1,090) or more." It includes the creation of a single rulebook and sets up a supervisory authority that will also have purview over the crypto sector. Read the full details HERE.

Speaking at a campaign speech in New Hampshire, Presidential Candidate Donald Trump said “I am also making another promise to protect Americans from government tyranny,” Trump said. “As your president, I will never allow the creation of a Central Bank Digital Currency. Such a currency would give the federal government, our federal government, absolute control over your money… They could take your money and you wouldn’t even know it was gone.” The Fed has made it clear on its website that it has made no decision on issuing a CBDC and would only proceed with issuance with an authorizing law. Federal Reserve Chair Jerome Powell testified before the House Financial Services Committee in March 2023 that a CBDC is “something we would certainly need Congressional approval for.”

In the Bitcoin ETF space, a Hong Kong Financial Services company, Venture Smart Financial Holdings Ltd, said it plans to lodge an application with the Securities and Futures Commission to launch a spot Bitcoin ETF. Brian Chan, the group head of investment and product said “Its a market that has huge potential”. Our goal is $500m in assets undermanagement by the end of this year.”

Charts of the Week

Because charts are just as important as macro.

The BTC:ETH correlation has dropped below its all time average of 0.71 for the first time since 2021. Hat tip to Kaiko Data for the chart.

What does sitting on cash cost you ? The average underperformance of cash vs S&P 500. Hat tip to Charlie Bilello for the chart.

Since the March 2023 liquidity injection, cash levels at large banks have trended up, while cash levels at small banks have trended down. Hat tip to Lyn Alden for the chart.

The MSCI China Index is about to go negative since its 1992 inception. Hat tip to Jake (@EconomPic) for the chart

Top Jobs in Crypto

Well, we all want to work in Crypto don’t we. Here’s a bit of help on your job search!

Crypto Trading Support Engineer at Hudson River Trading

Business Development Manager Crypto at Revolut

Director of Treasury at MoonPay

Associate, Growth, Payments and Platform Business Development at Coinbase

Head of Platform Security (Cloud DevSecOps) at Komainu

Legal Council, EMEA Regulatory at Blockchain.com

DISCLAIMER: The content in this newsletter is not financial advice. This newsletter is strictly educational and is not investment advice or a recommendation to buy or sell any assets or to make any financial decisions. Crypto markets are volatile, please be careful and do your own research.