Connecting the Dots

Episode 104 - Walking in a Bitcoin Wonderland

As we come to the last episode of 2024 we would like to wish all of our readers a Merry Christmas and Happy New Year!

Welcome to the new subscribers that have joined us over the last week. The aim of this newsletter is to help you navigate the world of crypto. There’s an incredible amount of information out there so we try to distil it into the things you MUST know each week, covering both macro and crypto.

For snippets and analysis on institutional crypto trading, give our X account a follow HERE.

Onto the newsletter. Here’s what you’re getting this week:

Macro Update: Our latest view on the macro and its impact on crypto markets.

Crypto Native News: The SEC approves the first combined BTC and ETH ETF, VanEck says the US debt could be significantly reduces with a Bitcoin Strategic Reserve.

Institutional Corner: The FCA publishes a discussion paper on crypto regulation, stablecoin market cap surpasses $200bn for the first time, Hong Kong grants licenses for 4 more crypto exchanges, Deutsche Bank developing an Ethereum Layer 2 network, El Salvador and the IMF reach an agreement.

Charts of the Week: BTC/EUR share of volume increasing, the Alameda liquidity gap closes, huge rise in Base TVL.

Top Jobs in Crypto: Featuring Galaxy, Ledger, Chainlink Labs, Ripple, Binance and LSEG.

Macro Update

This is where we connect the dots between macro and crypto.

Walking in a Bitcoin Wonderland

Just as the Santa rally looked in full swing, with Bitcoin hitting new record highs over $108k, Scrooge JPow poured a little cold water on festivities as the ghosts of inflation past spooked the Fed into delivering a hawkish FOMC.

Whilst cutting rates 25bps as expected, upward revisions to core inflation forecasts for 2025 from 2.2% to 2.5% led Fed members to revise lower expectations for rate cuts next year from four to two, in a decidedly more cautious FOMC.

Knee jerk saw broad risk dump, with equities and crypto sharply lower as US yields and the dollar raced higher. News on Thursday that the US economy grew at a revised 3.1% in Q3, outpacing the previous estimate of 2.8% reinforced the hawkish lean of markets, although Friday’s Core PCE inflation numbers, the Fed’s preferred inflation measure, held steady at 2.8% YoY with the MoM coming in just 0.1% Vs 0.3% expected, to return a little Christmas cheer.

What does this all mean?

In truth, this does little to alter the broadly supportive macro dynamic that has had us bullish Nasdaq and Bitcoin throughout 2024. Namely, we remain in a global rate cutting cycle with ample and rising liquidity. That liquidity is set to get a boost as China battles to escape a deflationary spiral, with a more “proactive fiscal” stance and looser monetary policy.

Furthermore, with Trump unsuccessfully negotiating a debt ceiling suspension as part of the spending bill to avoid a government shutdown, the US will be forced to draw down on over $750bn sat in their cash account at the Fed (the Treasury General Account (TGA)) This will be another huge liquidity/cash injection into markets which we expect to keep risk flying into Q1.

Once the debt ceiling is lifted/suspended (reminder that the US perpetually needs to raise/suspend the debt ceiling - nothing stops this train!) then liquidity will become more challenged as the US Treasury returns to the market, issuing new debt, rebuilding the TGA and sucking out cash. That’s when, all things equal, we expect crypto and broader risk will be vulnerable to a larger drawdown.

Until then, we view last week's moves as little more than a correction and wash out of over leveraged positions. Month/year end is also noisy as liquidity becomes challenged and PnL considerations dominate.

TLDR: Don’t read too much into this correction for risk. Conditions remain supportive.

Bitcoin and the broader crypto complex has typically performed well during the holiday season, so we’re still not ruling out a sharp recovery for Bitcoin to round out what has been a phenomenal year for digital assets, but this consolidation and leverage flush in the context of the large moves witnessed post US election, looks healthy. The paradigm shift in the US political and regulatory backdrop for digital assets is yet to be fully “priced” and we expect cash continues to flow into this space from across corporations, institutions and Sovereigns 👀

Unsustainable…

A continued move higher for US yields and the dollar does however pose risks for our bullish view, as the dollar wrecking ball can squeeze global liquidity and strangle risk assets. We don’t however feel these moves are sustainable.

The Fed is the de facto central bank for the world and with China leading a global slowdown, a stronger dollar and higher US yields is the last thing needed right now (it also runs counter to both Trump and incoming Sec Treasury Scott Bessent’s desire for a weaker dollar to facilitate global trade and reduce the US trade deficit.) The Fed will be forced to inject liquidity, supplying dollars at the first signs of “something breaking”.

Even closer to home, the Fed is aware of the potential difficulties in funding the US deficit. Indeed, the Fed cut the overnight repo rate on Wednesday by 30bps to align with the lower end of the Fed funds target rate and encourage a continued drain in the reverse repo facility (cash that is parked at the Fed overnight.) This now sits just below $100bn and will likely continue to flow out and into T-bills (more liquidity!) but once it approaches zero, the Fed will have little choice but to end Quantitative Tightening, reducing the supply of treasuries available in the market.

Remember, financial markets are not self-sustaining. They require ever increasing amounts of liquidity and financial repression in a game of whack-a-mole and ultimately, fiat currency becomes the escape valve. This is why we believe long term we will continue to see all hard assets rise in fiat currency terms. Bitcoin as the hardest asset will rise the most 💪

We also don’t believe the US data will support higher rates and this hawkish turn from the Fed looks ill-timed. The recent resilience and strength in the data is partly a function of the pre-election spend sugar high which is already starting to dissipate. Macro surprises are already rolling over, disappointing on the downside. The US labour market continues to display underlying softness whilst under the hood of inflation, core services inflation is easing with the lagged shelter costs still responsible for a large proportion of headline inflation. Market measures of inflation are also starting to come back lower, fading off the post election highs.

Just as we saw resilient US data in the spring quickly turn lower and force the 50bp rate cut, we believe the overly data dependent (read backward looking) Fed will be forced to flip flop back to a more dovish stance once again. Yields then look a little toppy to us here.

Overall, we maintain our bullish view for Bitcoin and broader risk heading into the new year. For markets which are a function of rates and liquidity, with a soft underbelly to global growth, we remain in a global rate cutting cycle, necessitating rising liquidity.

Bitcoin meanwhile, whilst following a familiar post-halving cycle, has an additional idiosyncratic narrative which is set to accelerate the secular trend, with the new US administration catalysing a global demand shock.

So as we raise a glass and celebrate an exceptional 2024, we also look forward to 2025 and the next leg for this bull market. We thank you, our readers, for being with us on this journey and wish you and your families a happy Christmas and all the best of health, happiness and Crypto for the new year 🥂

Native News

Key news from the crypto native space this week.

The Securities and Exchange Commission (SEC) has finally approved the first spot exchange-traded funds combining both Bitcoin and Ethereum. After several extended reviews since June this year the SEC has authorised Nasdaq to list the Hashdex Nasdaq Crypto Index US ETF and the Cboe BZX Exchange to list the Franklin Crypto Index ETF. The filing says that "The proportion of bitcoin and ether to be held by each Trust will be based on free-float market capitalisations." Senior Bloomberg ETF analyst Eric Balchunas expects the funds to launch in January with an approximate 80% Bitcoin and 20% Ethereum split, reflecting current market caps. The funds must comply with continued listing requirements and maintain transparency around portfolio holdings and pricing. Both exchanges will monitor compliance and can initiate delisting procedures if requirements aren't met. Trading in the ETF shares will be subject to existing equity securities rules on both exchanges. The funds will disseminate intraday indicative values every 15 seconds during regular trading hours.

Asset Manager VanEck said in its latest blog post that the U.S. could significantly reduce its national debt by as much as 36% through to 2050, if it adopts a Strategic Bitcoin Reserve. This initiative aligns with Senator Cynthia Lummis’s Bitcoin Act, which advocates for the US to amass 1 million bitcoins within the next five years. VanEck’s analysis supports this strategy, predicting that such an investment could cut national liabilities by an estimated $42 trillion by 2049. This projection assumes a consistent debt growth rate of 5% and an annual bitcoin appreciation rate of 25%. In this scenario, Bitcoin’s value would rise to over $42 million! Read the full report from VanEck HERE.

Institutional Corner

Top stories from the big institutions

The Financial Conduct Authority published a discussion paper published this week and asked for responses online by 14 March 2025. The paper asks for feedback on its planned regulation of cryptocurrencies. The regulator set out a number of objectives as part of proposals to “reduce risks without stifling growth and innovation”.

It said it aims to:

Improve regulatory clarity so there are clear and consistent ‘rules of the game’ for firms and consumers.

Make sure consumers have the information they need before buying or selling cryptoassets.

Require controls and processes to bring about fair and orderly trading conditions.

Reduce risks of money laundering and losses to fraud.

Read full details from the FCA HERE.

The latest CCData stablecoin and CBDC report was out this week. The report shows that in December, the total market capitalisation of stablecoins increased by 5.51% to reach $203bn, surpassing the $200bn milestone for the first time in the asset class’s history. This marked the fifteenth consecutive month of growth in the stablecoin market capitalisation. Year-to-date, the total market capitalisation of stablecoins has risen by 56.0%, up from $130bn. Other key findings include that USDT continues to dominate stablecoin trading. November saw a significant rise in Tether (USDT) dominance in stablecoin trading activity on centralised exchanges, with its market share increasing to 86.3% among the top stablecoins. FDUSD retained its position as the second most traded stablecoin, capturing 6.85% of the market share. The market capitalisation of Tether (USDT) rose by 4.51% in December, reaching $140bn—a new all-time high for the stablecoin. This marks the sixteenth consecutive month of growth in USDT’s market capitalisation. Circle’s USD Coin (USDC) saw its market capitalisation grow by 6.7% in December, reaching $42.4bn—its highest level since December 2022. Access the full report HERE.

Hong Kong has granted licenses to four more crypto exchanges as the region focuses on accelerating the licensing process amid growing competition to become a crypto hub. The Securities and Futures Commission said it approved licenses for four additional exchanges — HKbitEX, Accumulus, DFX Labs, and EX.IO — on Wednesday under its “swift licensing process” after the applicants addressed feedback from the regulator’s on-site inspections. The SFC has previously issued three such licenses to OSL, HashKey and HKVAX. Eric Yip, the SFC’s Executive Director of Intermediaries said in a statement Wednesday “We have been proactively engaging with VATPs’ senior management and ultimate controllers, which helps drive home our expected regulatory standards and expedite our licensing process for VATPs.” In a separate circular released Wednesday, the SFC provided more details on a revamped licensing process. In addition to on-site inspections, the regulator requires applicants to undergo assessments of their platform policies, procedures, systems and controls, which a certified public accountant must sign off. They added “The SFC will supervise the whole second-phase assessment process through a tripartite engagement with the VATPs and their external assessors and will uplift the restriction on business scope after the second-phase assessment is completed to the SFC’s satisfaction.”

Deutsche Bank is developing an Ethereum layer 2 network using ZKsync technology to enhance transaction efficiency and meet regulatory standards in finance. The initiative, part of Project Dama 2 and linked to Singapore’s Project Guardian, is aimed at resolving key issues for regulated lenders operating on public blockchains, such as unknown transaction validators, risks of payments to sanctioned entities, and unexpected hard forks. The goal is to enable banks to safely and securely utilise public blockchains for various financial services while addressing regulatory concerns, said Boon-Hiong Chan, Head of APAC Securities Market and Technology Advocacy at Deutsche Bank. The L2 solution will enable banks to create a “more bespoke list of validators” and provide regulators with “super admin rights” to monitor fund movements, he added.

El Salvador and the International Monetary Fund have reached an agreement for the country to limit domestic bitcoin-related activities in exchange for a financing package. The IMF’s Extended Fund Facility, which is expected to extend over the course of 40 months, includes a $1.4 billion loan to back El Salvador’s reform agenda and address the country’s balance of payment needs. The IMF said that with additional financial support expected from the World Bank, the Inter-American Development Bank, and other regional development banks, the total financing package is expected to be worth over $3.5 billion. In a statement the IMF said “Recognising El Salvador’s pending macroeconomic and structural challenges, the IMF-supported program aims to strengthen fiscal and external stability and help create the conditions for stronger and more inclusive growth.” Read the full release from the IMF HERE.

Charts of the Week

Because charts are just as important as macro.

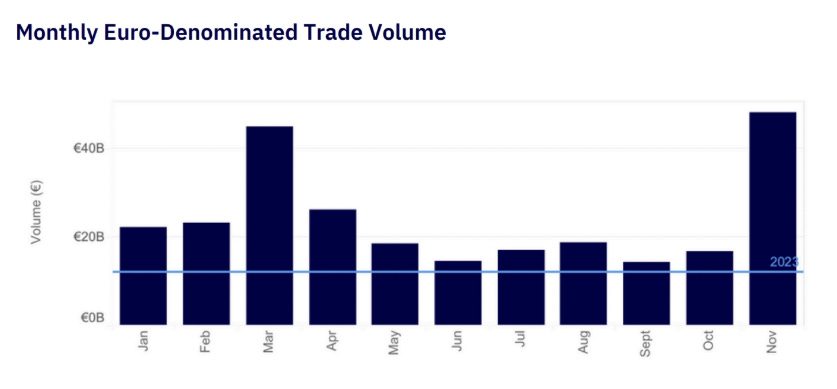

BTC/EUR's share of global Bitcoin-Fiat volume increases to 10% from 3.6% at the beginning of the year.

The ‘Alameda Gap’ – the crypto liquidity shortfall from FTX’s collapse – closed in 2024 as spot BTC ETFs helped boost market depth. Hat tip to Kaiko Data for the chart.

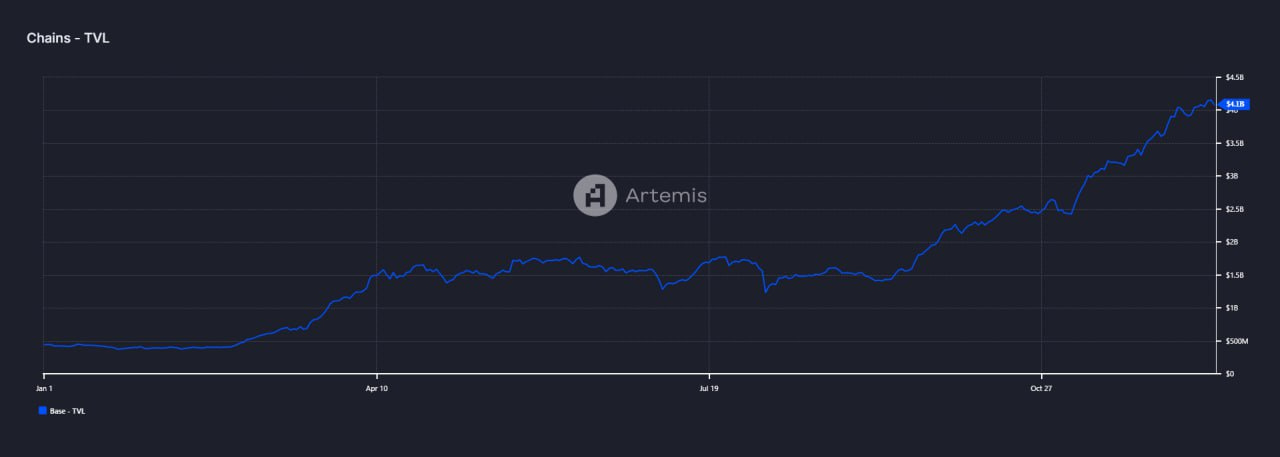

The TVL value of the Base increased from $438 million at the beginning of the year to $4.2 billion in December.

Top Jobs in Crypto

Well, we all want to work in Crypto don’t we. Here’s a bit of help on your job search!

2025 Sales and Trading Intern at Galaxy

Customer Support Specialist at Ledger

Senior Solutions Engineer, Banking and Capital Markets at Chainlink Labs

Senior Sales Manager for Crypto Natives at Ripple

Binance Accelerator Program - Binance Academy Editor at Binance

Digital and Securities Market COO at London Stock Exchange Group (LSEG)

DISCLAIMER: The content in this newsletter is not financial advice. This newsletter is strictly educational and is not investment advice or a recommendation to buy or sell any assets or to make any financial decisions. Crypto markets are volatile, please be careful and do your own research.