Connecting the Dots

Episode 81 - Flow State

Welcome to the new subscribers that have joined us over the last week. The aim of this newsletter is to help you navigate the world of crypto. There’s an incredible amount of information out there so we try to distil it into the things you MUST know each week, covering both macro and crypto.

For snippets and analysis on institutional crypto trading, give our X account a follow HERE.

Onto the newsletter. Here’s what you’re getting this week:

Macro Update: Lots going on in the macro, closely watching the DXY, yields and China. The macro continues to unfold nicely to support a continued bull market for Bitcoin.

Crypto Native News: Circle acquires European EMI license, BitMEX launces a memecoin index, Chainlink partners with Fidelity and Sygnum

Institutional Corner: South Korea’s Financial Supervisory Service launces a 24 hour surveillance system, Sony to launch a crypto exchange.

Charts of the Week: DXY has the biggest correlation to bitcoin, stablecoin share of volume increased, large bitcoin hashrate drawdown.

Top Jobs in Crypto: Featuring Quant Capital, Blockchain.com, Uphold, Fidelity Digital Assets, Binance, Copper and Kraken.

Macro Chart of the Week - US Treasury term premia jumped thru' late-June. Hat tip to Cross Border Cap for the chart.

Macro Update

This is where we connect the dots between macro and crypto.

Flow State

A difficult week for Bitcoin culminated in a Friday flush, taking us briefly below $53,500 before recovering into the weekend. Negative flow drivers dominating otherwise constructive developments on the macro.

Those negative flow drivers are dominated by the Mt Gox distribution, with $2.6bn of the circa $8bn distributed on Friday, whilst the German Government also continues to sell down holdings, up to $175mio on Thursday. According to Blockworks, both the US and German governments have sent $738m worth of Bitcoin to exchanges over the past two weeks. Given the holiday thinned liquidity and general market apathy into the summer, this was enough to drive the largest liquidation since the FTX collapse in 2022 😳

Perhaps it’s worth noting, it was the FTX liquidation event that marked the lows from which Bitcoin began its bull market recovery. Maybe this was the flush markets needed to shake us out of our malaise and bring attractive levels for longer term bulls to re-engage. Friday’s net ETF inflows of $143bn provide some encouragement!

September rate cut…

Digging into the macro, the soft US data pulse continued, underscored by the services ISM which plunged into contraction territory, falling from 53.8 to 48.8, its lowest level since shortly after the Covid lockdowns in 2020. New orders also fell into contraction territory alongside falling employment whilst price pressures eased from 58.1 to 56.3. The service sector is starting to “catch down” to the still beleaguered manufacturing sector in the US.

Non farm payrolls also revealed a softening trend in the labor market. Despite a headline beat of 206k Vs 191k expected, sizeable revisions to May and April from 272k to 218k and 165k to 108k respectively, plus a rise in the unemployment rate to 4.1% (highest since Nov 2021) will feed a sense of caution at the Fed. Additionally, the employment gains came entirely from the public sector, off-setting the weakness in the private sector. Once again, the apparent “resilience” of the US economy is being manufactured in a profligate Whitehouse.

As we’ve said before, the labor market is the most lagging of indicators and the biggest “up the stairs, down the elevator shaft” series. Once it starts to deteriorate, it can rapidly fall apart and signs abound that the labor market is starting to crack. Certainly, the Fed minutes showed little concern about conditions being too loose, with the discussion largely focused on the downside risks. JPow speaking at a central bankers gathering at Sintra also treading a dovish line, noting that inflation had made “quite a bit of progress back to 2%” and that the economy is “back on a disinflationary path.” He also noted the cooling in the labor market as it rebalances.

Combined with the latest read on the labor market, September is looking like a lock for the Fed to begin the rate cutting cycle, with the market back to fully pricing 2 cuts for 2024. This dovish repricing reflected in the front end, with 2yr yields dropping 15bps on the week to 4.60%, the lowest levels since April and pulling the entire curve lower, with 10yr back sub 4.30%.

Cross asset macro supportive…

We wrote last week about our expectation for a slowing US economy to see the US dollar and yields reverse and this week felt like that move got underway. Quite importantly, the dollar wrecking ball which continues to plague Asia and wider EM, showed signs of reversing along with yields, the broad dollar falling 1% on the week and testing some key trend line supports. This relieved some of the pressure on the Yuan, with USDCNH back sub 7.30 at 7.2860. We continue to hold the view that Bitcoin will struggle to significantly rally all the while the Yuan remains under pressure.

Continued relief on the Yuan however will need to come from a continued softening in the US as China’s economy shows no signs of reflating. Official manufacturing PMI’s at 49.5 in China suggesting the sector contracted for a second month in a row, whilst services are barely in expansion mode at 50.5, down from 51.1 in May. Meanwhile, despite the recent rescue package for the housing market, new home sales also fell 17% in June, albeit exhibiting a slower pace of decline.

Perhaps importantly for Bitcoin, China remains cautious in its stimulatory measures, refraining from bringing out more forcefully the liquidity hose. Maybe they’re trying to maintain stability ahead of the communist party’s Third plenum to be held on the 15th to 18th July, where President Xi will unveil plans to boost growth. Things could well get moving post that gathering.

Overall, the macro continues to unfold nicely to support a continued bull market for Bitcoin. Net global liquidity which has largely drifted sideways in Q2 is set to start increasing as the Treasury ramp up T-bill issuance and drain further the RRP which will act as a cash injection into markets through Q3. We believe too, post the Third Plenum in a couple of weeks, we’ll see a step up in stimulative measures in China. Having been in “macro purgatory” with Fed rate cuts pushed out, we are now about to see the rate cutting cycle get under way in September, something the Fed will lead the market into, delivering us out of macro purgatory, into macro heaven.

For those new to Bitcoin, it would have been a concerning week. Yet these drawdowns of 25% from the highs are a typically common part of the bull market journey in a 70 vol asset class. The macro cycle however, governs the crypto cycle and we remain on track there.

It’s always difficult to catch a falling knife and if there’s persistent “real” selling without the off-setting real demand, then the risks remain that Bitcoin can stay heavy in the short term. Yet Friday’s capitulation and subsequent bounce, alongside the RSI’s in oversold territory auger well for a recovery from here and for Bitcoin to reconnect with the macro fundamentals which this week, continued to evolve favourably. This looks a great set up for long term investors to BTFD 💪.

Native News

Key news from the crypto native space this week.

As MiCA went live on Monday, Stablecoin issuer Circle announced that it had secured an Electronic Money Institution (EMI) license, a prerequisite to offering dollar- and euro-pegged crypto tokens in the European Union under the Markets in Crypto-Assets (MiCA) regulatory framework. Armed with an EMI license from the French banking regulatory authority, Circle Mint France will “onshore” the issuance of its euro-denominated EURC stablecoin to the EU and issue USDC for customers in the 27-nation trading bloc from the same entity.

Derivatives cryptocurrency exchange BitMEX has launched the MEMEMEXTUSDT Basket Index Perpetual Swap Contract offering traders exposure to the top 10 memecoins in the market through a single contract. The BitMEX memecoin basket index is constructed as a weighted average price of the top 10 memecoins by market capitalisation, with the index constituents rebalanced monthly to ensure it continues to track the best-performing memecoins. It is a USDT-margined linear perpetual swap offering up to 25x leverage. BitMEX said the multiple-memecoin contract can also "provide improved liquidity, enabling traders to more easily execute their trades at favourable prices."

Decentralised computing platform Chainlink today announced a collaboration with Fidelity International and crypto bank Sygnum on a project that focuses on bringing net asset value data onchain. The partnership aims to provide transparency and accessibility for NAV data in tokenised assets, specifically Sygnum’s recently issued onchain representation of $50 million Matter Labs’ treasury reserves held in Fidelity's $6.9 billion Institutional Liquidity Fund. Chainlink said in the release that its technology facilitates the secure storage and automated synchronization of NAV data for these tokens on the ZKsync blockchain, which is a member of Chainlink’s SCALE program. Chainlink added that its chain-agnostic approach helps to distribute data securely across various blockchain networks or offchain systems.

Institutional Corner

Top stories from the big institutions

South Korea’s Financial Supervisory Service announced today that it has developed a 24-hour surveillance system with local exchanges that will screen for any suspicious activity in the cryptocurrency market. The new system is set to go live on July 19, the day South Korea’s first regulatory framework for crypto investor protection comes into effect. From January to May this year, the FSS said it prepared a standardised reporting format for transaction data submissions from local exchanges, upon which it built a system that separates irregular transactions from the rest. The press release said “We benchmarked KRX's (Korea Exchange) criteria in extracting abnormal transactions and prepared models and metric indicators through several simulations, which we expect will filter out abnormal transactions meticulously.” Read the full statement from FSS HERE.

Japan’s multi-industry conglomerate Sony is getting ready to launch a cryptocurrency exchange subsidiary by revamping local trading platform WhaleFin which it acquired last year. WhaleFin has been renamed to S.BLOX Co., which plans to collaborate with Sony Group’s other businesses to generate additional value for its crypto trading services, according to the statement. The revamp also includes a redesign of the user interface and a new mobile app that will be easier to use, the release said. The exact launch date of S.BLOX crypto exchange has not been announced.

Charts of the Week

Because charts are just as important as macro.

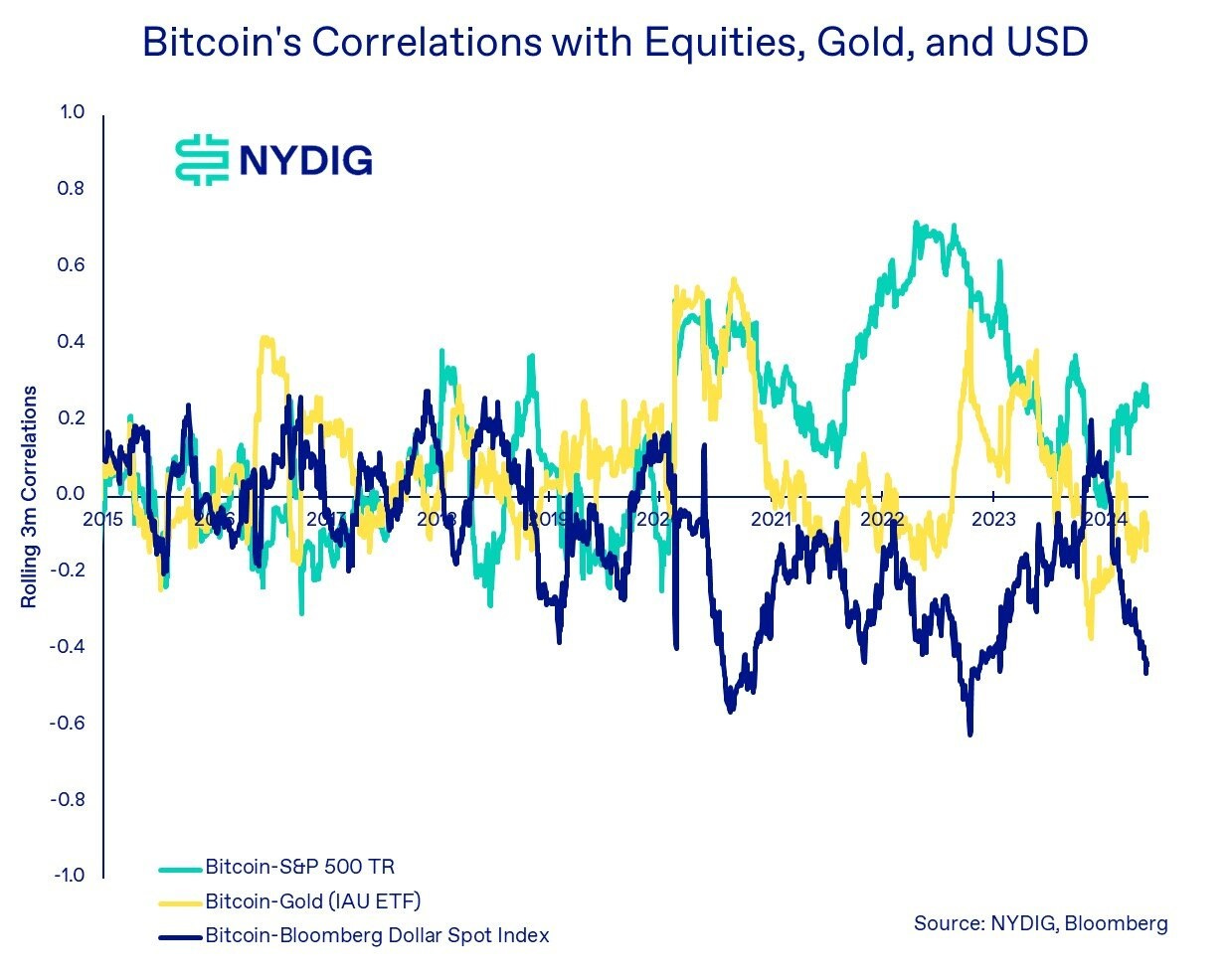

The US dollar index has been much more important for correlations to bitcoin than equities. Hat tip to Nydig for the chart.

The share of stablecoins vs fiat just hit its highest level since 2020. Currently, 84% of crypto trade volume involves stablecoins, while fiat accounts for only 16%. Hat tip to Dessislava Ianeva for the chart.

Bitcoin network true hashrate drawdown has reached the same level as post FTX. Hat tip to Quinten Francois for the chart.

Top Jobs in Crypto

Well, we all want to work in Crypto don’t we. Here’s a bit of help on your job search!

Junior Cryptocurrency Trader at Quant Capital

Controller, EMEA for Blockchain.com

Director, Business Development at Fidelity Digital Assets

Java Development Lead - Core Platform at Binance

Senior Software Engineer (Blockchain) at Copper

DISCLAIMER: The content in this newsletter is not financial advice. This newsletter is strictly educational and is not investment advice or a recommendation to buy or sell any assets or to make any financial decisions. Crypto markets are volatile, please be careful and do your own research.