Connecting the Dots

Episode 109 - Climbing the Wall of Worry

Welcome to the new subscribers that have joined us over the last week. The aim of this newsletter is to help you navigate the world of crypto. There’s an incredible amount of information out there so we try to distil it into the things you MUST know each week, covering both macro and crypto.

For snippets and analysis on institutional crypto trading, give our X account a follow HERE.

Onto the newsletter. Here’s what you’re getting this week:

Macro Update: Our latest view on the macro and its impact on crypto markets.

Crypto Native News: Coinbase has obtained its VASP registration in the UK, BlackRock disclosed that it now owns 5% of Strategy and VanEck suggests SOL may hit $520 by the end of 2025.

Institutional Corner: The Hong Kong Securities and Futures Commission adds headcount for crypto staff, the CFTC announces a forum for crypto CEO’s.

Charts of the Week: Change in market share for spot and derivatives, Bitcoin’s annual volatility fell to an all-time low.

Top Jobs in Crypto: Featuring DRW, Kraken, Keyrock, LSEG, Galaxy Digital and Nonco.

Macro Update

This is where we connect the dots between macro and crypto.

Climbing the Wall of Worry

As we warned in last week’s Connecting the Dots, markets endured a volatile week, with risk initially selling off hard on Trump’s announcement of 25% tariffs on neighbouring Canada and Mexico, only to reverse losses as those tariffs were said to be postponed with Mexico and Canada seeking to address the concerns on drug trafficking and border security. After selling off circa 2% on Monday, the S&P 500 ended the week pretty much flat.

Bitcoin meanwhile as a higher beta risk proxy ended the week down circa 6%, having at one point been down 11% after the biggest liquidation event in crypto history. That’s some feat when we consider the events of 2022 with the FTX blow up and the Covid liquidation in 2020 🤯

Historically, such liquidity cascades have marked local lows and perhaps, after a period of choppy sideways price action, was the cleansing flush needed to begin the next leg higher of this bull market.

Certainly we feel the macro cycle continues to be supportive of such. Indeed, as we expect 30%+ corrections during a typical bull run for Bitcoin, we’re encouraged by Bitcoins resilience which is a nod to the “real” underlying institutional demand which continues to flow into this market post the US election 💪

Macro on track…

On the macro, the Bank of England continued the global rate cutting theme, cutting rates 25bps as expected. Growth forecasts were also slashed from 1.5% to 0.75% for this year (although inflation revised higher) and in a dovish twist, 2 members actually voted for a 50bp cut, including Catherine Mann who was a hawkish member of the committee in 2024 and was expected to vote for a hold. The market still feels under priced for cuts across major central banks in 2025!

In the US meanwhile, ISM data kicked off a busy data week, revealing manufacturing eked out some expansion in January for the first time since 2022, however, the more important service ISM slowed from 54 to 52.8. Still in expansion territory, but in keeping with our expectation for a simmering economy post the pre-election spending sugar high ✅

Signs of a cooling labour market were also apparent this week. The headline data release, non farm payrolls, was somewhat mixed, with a weaker headline print coming in at 143k, down from an upwardly revised 307k, but unemployment ticking lower to 4%. Average earnings remained flat at 4.1%. Greater signs of slack however came from the JOLTS survey which showed that US job vacancies fell to 7.6 million in December, below consensus and down from November’s 8.16 million, to register the lowest level since September. Labour market slack continues to grow and as JPow noted in last week's FOMC, the labour market is not a current source of inflation. Indeed, BLS revisions to the 2024 guestimates were revised some 600k lower, suggesting the labour market was not as strong as thought last year.

We remain on track then for further Fed rate cuts amidst a broader global easing cycle and rising liquidity which keeps us firm in our bullish view for Bitcoin, crypto and broader risk assets in 2025. The explosive move higher for Bitcoin is still ahead 💥

US yields and dollar tailwinds…

Two macro factor inputs we remain very focused on is the US dollar and US yields, particularly given the important role they play for global financial conditions and liquidity. With the dollar and yields spiking post the election, Bitcoin has been rising in the face of these macro headwinds given the positive demand shock resulting from a crypto friendly administration, as well as a still positive global liquidity story with central banks easing and China pumping stimulus.

However, we expected yields and the dollar to fade, both on the fading US reflation story as well as an unwind of the knee jerk “Trump Trade” and for the headwinds to flip into powerful tailwinds for Bitcoin in 2025. Both appear to have topped out in a “sell the news” fashion on the inauguration and have been moving lower, despite the tariff induced volatility.

Potentially very important comments that are also worth noting, came this week from Treasury Secretary Scott Bessent. He said in an interview that the Trump administration’s focus on getting down borrowing costs is on 10yr yields, rather than the Fed funds rate per se. The path to achieving this will be via an expansion of the energy supply (lower oil) to help reduce inflation expectations as well as cutting spending and promoting non-inflationary growth. Bessent describes his economic policy as the 3-3-3. Fiscal deficits back to 3% (from current 7%), increase oil production by 3mio b/d and sustain economic growth at 3%.

Trump and Bessent want lower yields, a weaker dollar, weaker oil, higher stocks and now higher Bitcoin. Currently they’re making good progress on oil, yields and the dollar which since the inauguration are down 10%, 30bps and 1.3% respectively. The mistake people make on Trump is in thinking it’s all random chaos. Yet Trump is very clear on his goals, and alongside Bessent, has a plan to achieve those.

Our expectation then is that the market, which has the Trump Trade “wrong way round” will recalibrate over the coming weeks and we continue to see the dollar and US yields moving lower, creating a huge tailwind for Bitcoin and broader risk. The path to that however will be a volatile one as Trump continues to use the stick of tariffs before agreements are made and there’s global co-operation to help get the dollar and yields lower, to stimulate global growth.

TLDR; The macro remains on track for the next leg higher of this crypto bull market. Don’t be shaken out by the short term, tariff induced noise which is a means to an end for an administration looking for a weaker dollar and lower yields. Markets have climbed a wall of worry in the past 2 weeks with DeepSeek and Tariff fears. Bitcoin is battle hardened and ready to take the next leg higher 🚀

Native News

Key news from the crypto native space this week.

Coinbase has obtained its VASP registration in the UK. Issued by the FCA, this will allow Coinbase to offer both crypto and fiat in the UK, the largest of Coinbase’s international markets, as the company secures another regulatory permission. This VASP registration makes Coinbase the largest registered digital assets player in the UK. Coinbase said “The UK Government and the FCA are developing welcome regulation for the crypto sector, hopefully joining the growing trend of countries embracing economic freedom and free markets. Governments around the world are waking up to the fact that crypto fuels economic prosperity. We believe that crypto is the most important technology that can generate growth in the world, and the UK is poised to benefit from this. This is a critical registration to cement our strong position in the UK and unlock our ambitious expansion plans. Our mission is to onboard the next 1 billion people into crypto while prioritising security for customer assets and maintaining the highest standards of compliance. Coinbase’s core thesis is that greater adoption and use of cryptocurrencies will increase economic freedom, and achieving our VASP in the UK furthers this belief.” Read the full announcement from Coinbase HERE.

In a recent Schedule 13G filing, BlackRock disclosed that it now owns 5% of Strategy (MSTR), equivalent to approximately 11.2 million shares. This marks a 0.91% increase from its previous 4.09% ownership as of September 30, 2024. A Schedule 13G is filed when an investor acquires more than 5% of a publicly traded company’s stock but does not intend to influence or control the company. Institutional investors must file within 45 days after year-end or within 10 days if ownership exceeds 10%. See the full filing HERE.

Investment firm VanEck predicts Solana's SOL will touch $520 by the end of 2025 as the demand for smart contract platforms (SCP) grows and M2 money supply increases in the coming months. VanEck predicts M2 money supply will grow to $22.3 trillion by 2025 from the current $21.5 trillion. The SCP market is where platforms like Solana operate, allowing for the creation and execution of smart contracts — which VanEck estimates could grow by 43% to reach $1.1 trillion by the end of 2025. Currently, Solana holds about 15% of this market, but VanEck expects this will rise to 22% by the end of 2025. VanEck said “Using an autoregressive (AR) forecast model, we estimate Solana’s market cap will reach ~$250B, implying a SOL price of $520 based on ~486M floating tokens,” it added. An autoregressive (AR) forecast model looks at past data to predict future values.

Institutional Corner

Top stories from the big institutions

The Hong Kong Securities and Futures Commission has proposed adding headcount for cryptocurrency specific staff. In a budget plan for the financial year 2025 to 2026, the Securities and Futures Commission proposed 15 new headcounts, with eight dedicated to “enhancing the staffing support for virtual asset regulatory regimes, market surveillance, and enforcement investigations.” The SFC presented the budget this week at a Legislative Council meeting. The regulator estimated that its recurrent expenditure for the next fiscal year—starting April 1, 2025—would be HK$2.59 billion ($332.4 million), an increase of 7.2% from the forecast expenditure for 2024-25. Much of the budget increase stems from a rise in staff costs by HK$130.5 million ($16.7 million), which includes an average salary hike of about 2.1%. The SFC noted that it froze its headcount in three out of the five financial years since 2020-21.

The Commodity Futures Trading Commission (CFTC) has announced a forum for crypto industry CEOs to provide input on an upcoming digital asset pilot program. According to the CFTC, the pilot program will explore “tokenised non-cash collateral,” which includes stablecoins and similar products. CEOs from stablecoin issuer Circle, centralised exchanges Coinbase and Crypto.com, and blockchain firm Ripple will attend the forum. Acting CFTC Chairman Caroline Pham said continued engagement with the crypto industry would pave the way toward fulfilling the Trump administration’s pro-crypto promises.

Charts of the Week

Because charts are just as important as macro.

Change in Spot market share. Bybit and Binance made the largest gains in market share, rising 1.02% and 0.83% to 7.65% and 26.2% respectively. Hat tip to CCData for the chart.

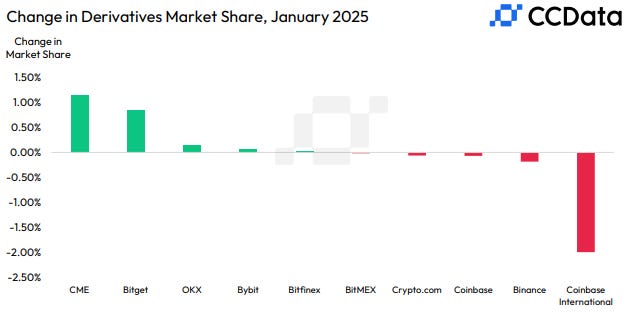

CME and Bitfinex were the best-performing derivatives exchanges based on month-on-month change, with their volumes increasing by 7.81% and 6.30% to $285bn and $7.55bn, respectively. Among the 16 derivatives exchanges, Binance leads with a market share of 39.7% of total volumes in January. This was followed by OKX with a market share of 16.4% and Bybit with a dominance of 15.9%.

Bitcoin’s annual volatility fell to an all-time low, while its risk-adjusted returns remained superior to most major asset classes.

Top Jobs in Crypto

Well, we all want to work in Crypto don’t we. Here’s a bit of help on your job search!

Senior Associate Business Development Asset Listing at Kraken

Trading Assistant - Crypto Options at Keyrock

Product Manager, Digital Assets at LSEG

Sales Support Analyst – Liquidity Provision/Market Making at Galaxy Digital

DISCLAIMER: The content in this newsletter is not financial advice. This newsletter is strictly educational and is not investment advice or a recommendation to buy or sell any assets or to make any financial decisions. Crypto markets are volatile, please be careful and do your own research.

great newsletter, as always, especially excited to see what Bessent will deliver